Budgeted Income

Topic 2

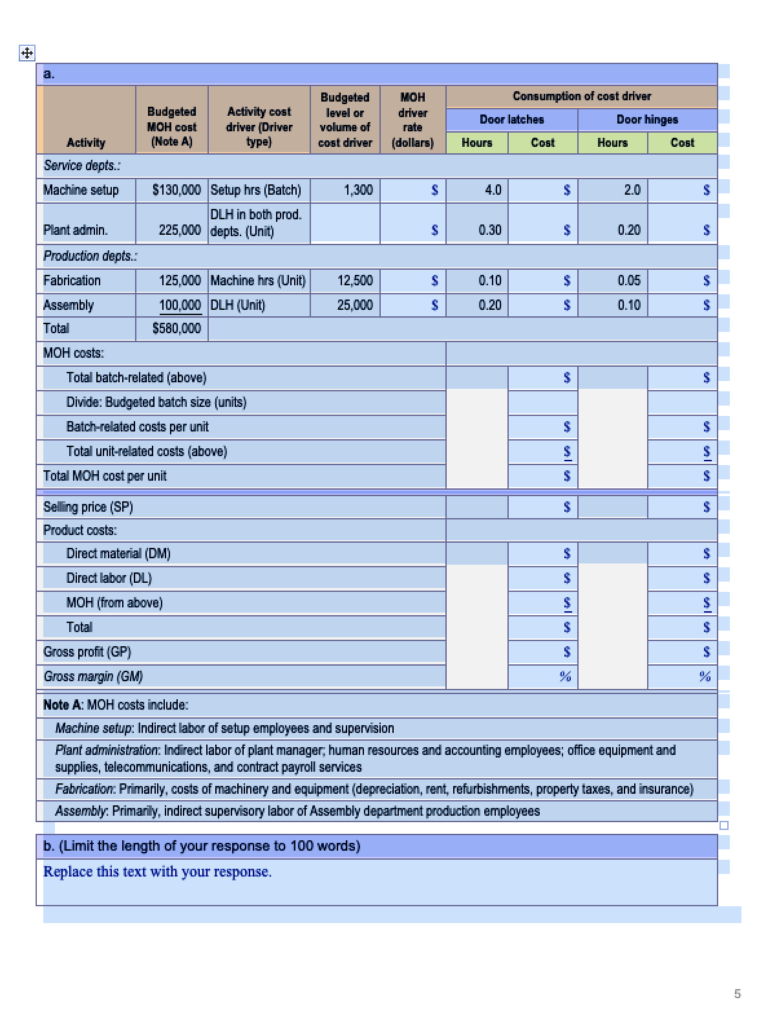

The board of directors of Mercury Manufacturing Company recently approved the company’s budget and production plan for its coming fiscal year (FY). The company manufactures two products – door latches and door hinges – from a single plant that comprises four activities – machine setup, fabrication, assembly, and plant administration. The company uses the same resources (including machinery and equipment, supervision and administrative services) to manufacture both products. Management uses the traditional approach to allocate manufacturing overhead (MOH) costs, based on direct labor hours (DLH) incurred in its two production departments, to determine the unit cost of each product. The company’s budget includes the following MOH allocation and related computations:

| Per unit: | Door latches | Door hinges | ||

| Selling price (SP) | $24.75 | $11.98 | ||

| Product costs: | ||||

| Direct material (DM) | $ 7.20 | $ 2.90 | ||

| Direct labor (DL) | 7.50 | 5.00 | ||

| MOH (A) x (B) | 3.87 | 2.58 | ||

| Total | $18.57 | $10.48 | ||

| Gross profit (GP) | $ 6.18 | $ 1.50 | ||

| Gross margin (GM) GM = GP / SP (see Note 1 below) | 25.0% | 12.5% | ||

| Budgeted total units of production for fiscal year (FY) | 50,000 | 150,000 | ||

| Budgeted batch size (units per batch) | 200 | 1,000 | ||

| (A) Direct labor hours (DLH) per unit | 0.30 | 0.20 | ||

| (B) MOH cost per direct labor hour (DLH) | (C) | $12.90 | (C) | $12.90 |

| (C) Budgeted FY total MOH cost, $580,000 / Budgeted FY total DLHs, 45,000 |

Management is considering adopting the Activity-based Costing (ABC) method to determine its product unit costs.

- Using the information included in the table below (taken from the company’s budget and production plan) complete the table according to the ABC method to compute the per-unit MOH cost, total cost, gross profit, and gross margin of each product.

- Describe briefly the apparent effect that managers’ use of the traditional MOH allocation method has had on its pricing decisions, compared to using the ABC method.

The budget and production plan reflect normal levels of production resource availability and capacity utilization (i.e., activity resource consumption) for the company.

For solution towards the above problem email: [email protected] or chat with us on live .